Wealth Accumulation – Thought Process & Financial Planning Tool

Wealth Accumulation

Let’s have a right understanding of why wealth accumulation is important. If one does not need wealth accumulation, then what ever one earns will go towards immediate spending. Common sense will alert one that this is not wise. Wealth accumulation is the deliberate and discipline process of accumulating assets to achieve certain meaningful goals. Without a clear goal, wealth accumulation is no different with wealth hoarding, produces more stresses and anxieties. We accumulate wealth for the following three generic goals:

In the next section, we will discuss deeper the three generic goals and the appropriate types of assets for wealth accumulation in Singapore’s context.

Wealth Accumulation – Three Generic Goals & Types of Assets

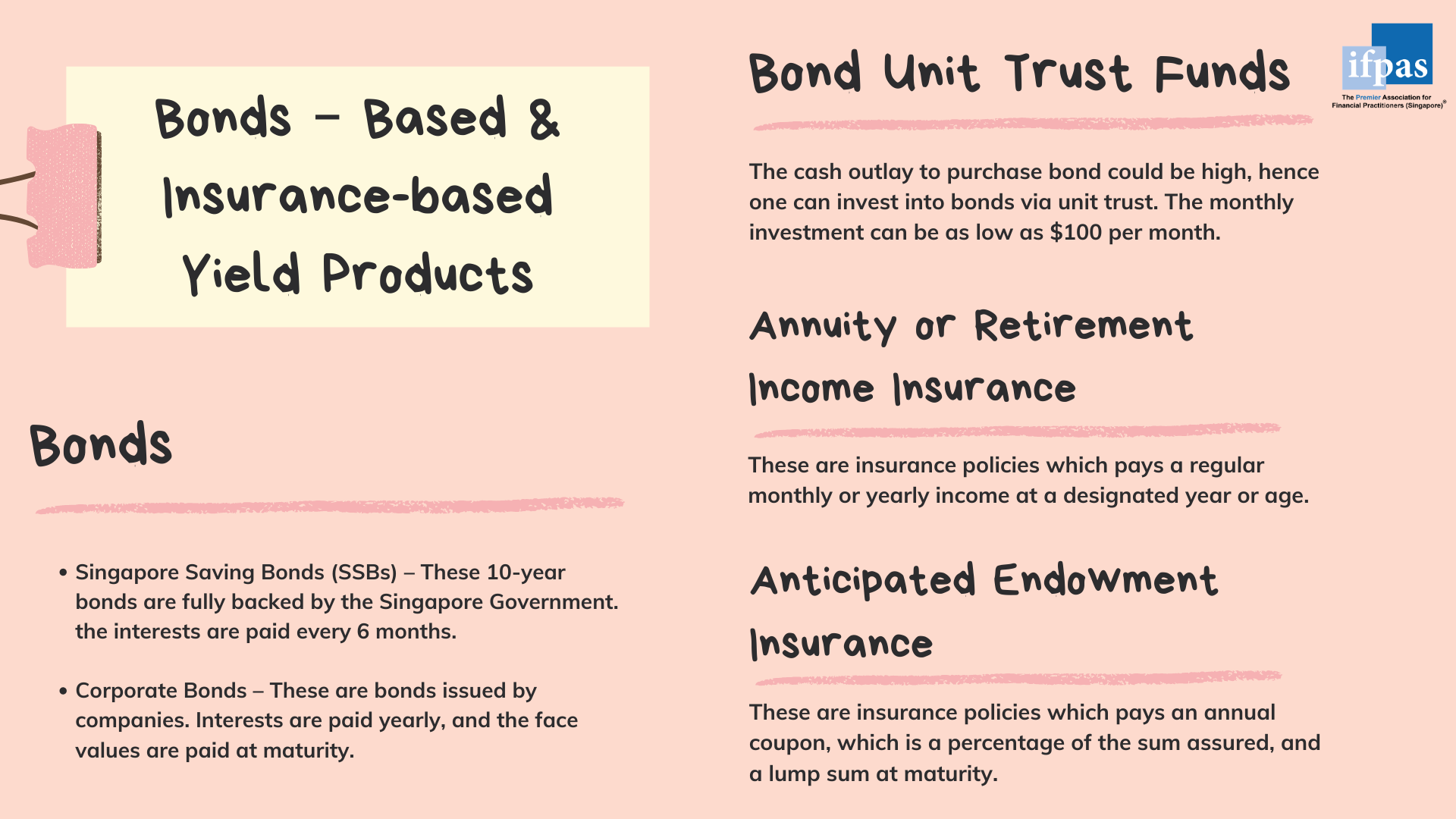

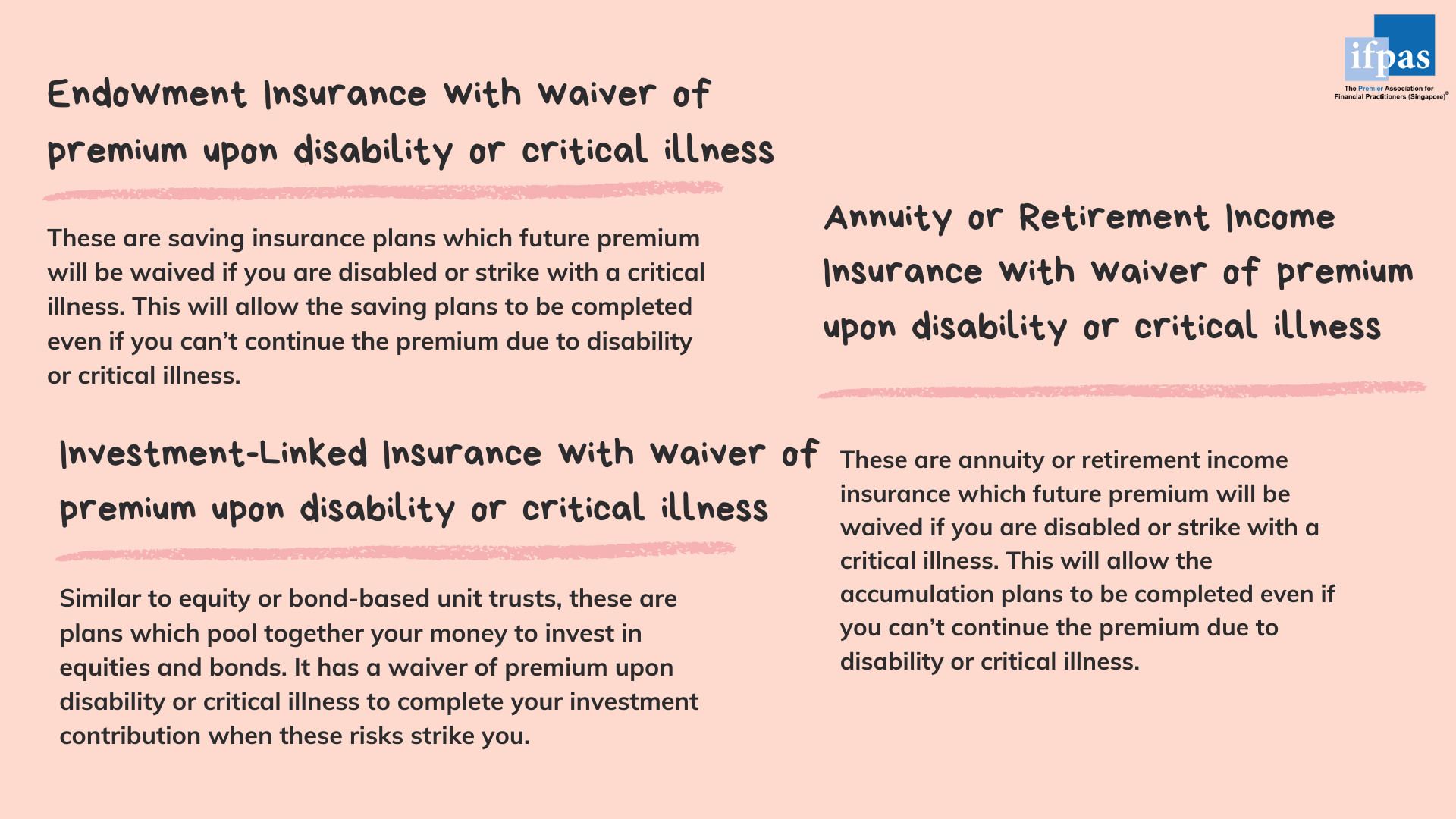

There are various tools to accumulate wealth. Care, discernment and discipline are required. We will use above three generic goals to describe the appropriate tools.

Step 1 – Have a realistic time horizon for the purchase and expectation of property types. As in all financial planning, the first step is to set expectation and formulate goal. Due to the property price, it is necessary to set a longer time horizon for the purchase. In Singapore, there are public housing and private properties. Public housing which is sold directly from HDB is actually affordable, however one must satisfy the qualifying conditions, for example, forming a family nucleus.

Step 2 – Understand the cost of acquiring property and save for it. There are 3 generic costs of acquiring property in Singapore. First, down payment, which is the most obvious and biggest amount. This can be in the region of 10% to 20% of the property price. Due to the relatively high price of property, one has to be realistic on the saving time horizon. It could be in the region of 5 to 10 years. Below is a table showing the numerical figures:

| Property Price (S$) | Down Payment 20% (S$) | Remarks |

| 250,000 | 50,000 | Build To Order (BTO) from HDB |

| 500,000 | 100,000 | HDB Re-sale Flat |

| 750,000 | 150,000 | Executive Condominium |

| 1,000,000 | 200,000 | Private Property |

| 3,000,000 | 600,000 | Landed Property |

The cost of acquiring property is high, but on close analysis, it is not unachievable. What is required is that one needs to have discipline and prioritise one’s financial goal (for example prioritising buying a property over buying a car, which is another very expensive item in Singapore). The table below shows the estimated amount saving needed to achieve the financial goal.

| Property Price (S$) | Down Payment 20% (S$) | Yearly Saving Required (S$) (Assumption: FD @ 1% p.a.) | |

| 5 YEARS | 10 YEARS | ||

| 250,000 | 50,000 | 9,705 | 4,732 |

| 500,000 | 100,000 | 19,410 | 9,464 |

| 750,000 | 150,000 | 29,114 | 14,195 |

| 1,000,000 | 200,000 | 38,820 | 18,927 |

| 3,000,000 | 600,000 | 116,459 | 56,781 |

Second, it is also important to budget another 5% to 10% of the property price as a gauge for renovation and furnishing the property. Third, one has to take note of the holding cost of property. For example, ongoing monthly conservancy fee, property tax, insurance and maintenance cost. These costs could be small and, thus, less visible compared to down payment, but they can be a strain on one’s finances collectively

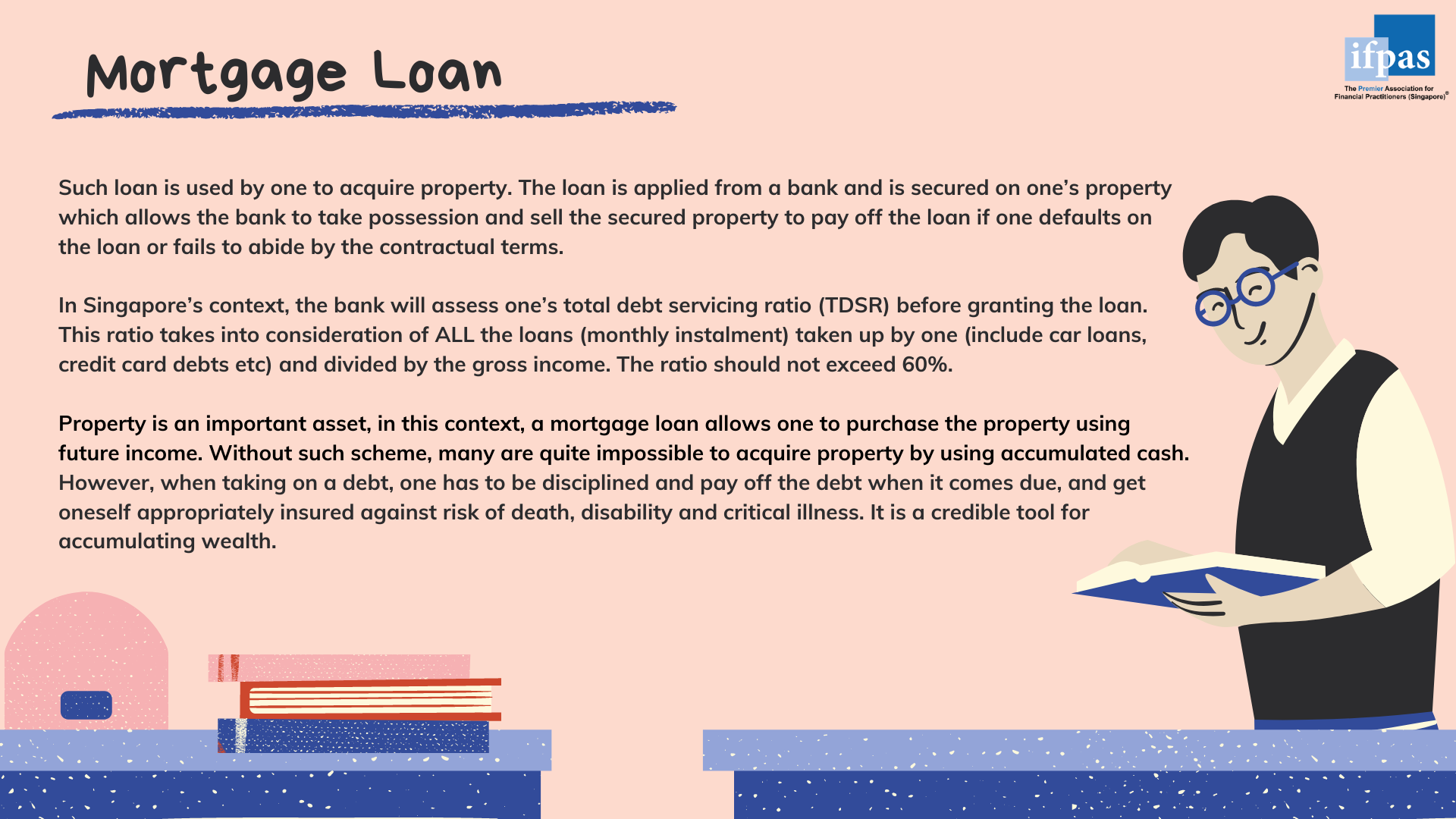

Step 3 – Mortgage loan and Total Debt Servicing Ratio (TDSR). As you can see, acquiring a property in Singapore requires significant financial resources, therefore, most of us will require debt to finance the acquisition. Such debt is known as mortgage loan, which will be explained further in the later part of this writing. One point to add at this point is that the Monetary Authority of Singapore (MAS) sets out a formula for banks to compute the total debt which a person can borrow. This is known as Total Debt Servicing Ratio (TDSR), which says monthly total debt obligations divided by gross monthly salary should not exceed 60% of your gross monthly income. The table below shows the estimated mortgage loan that one can borrow and the corresponding affordable property type.

| Monthly Income | Maximum TDSR 60% | Max Mortgage Loan (30 years tenure @ 3.5%) | Affordable Property Type |

| $2,500 | 1,500 | $334,042 | HDB BTO flat |

| $5,000 | 3,000 | $668,085 | HDB re-sale flat |

| $7,500 | 4,500 | $1,002,127 | Small-size private condo |

| $10,000 | 6,000 | $1,336,170 | Mid-size private condo |

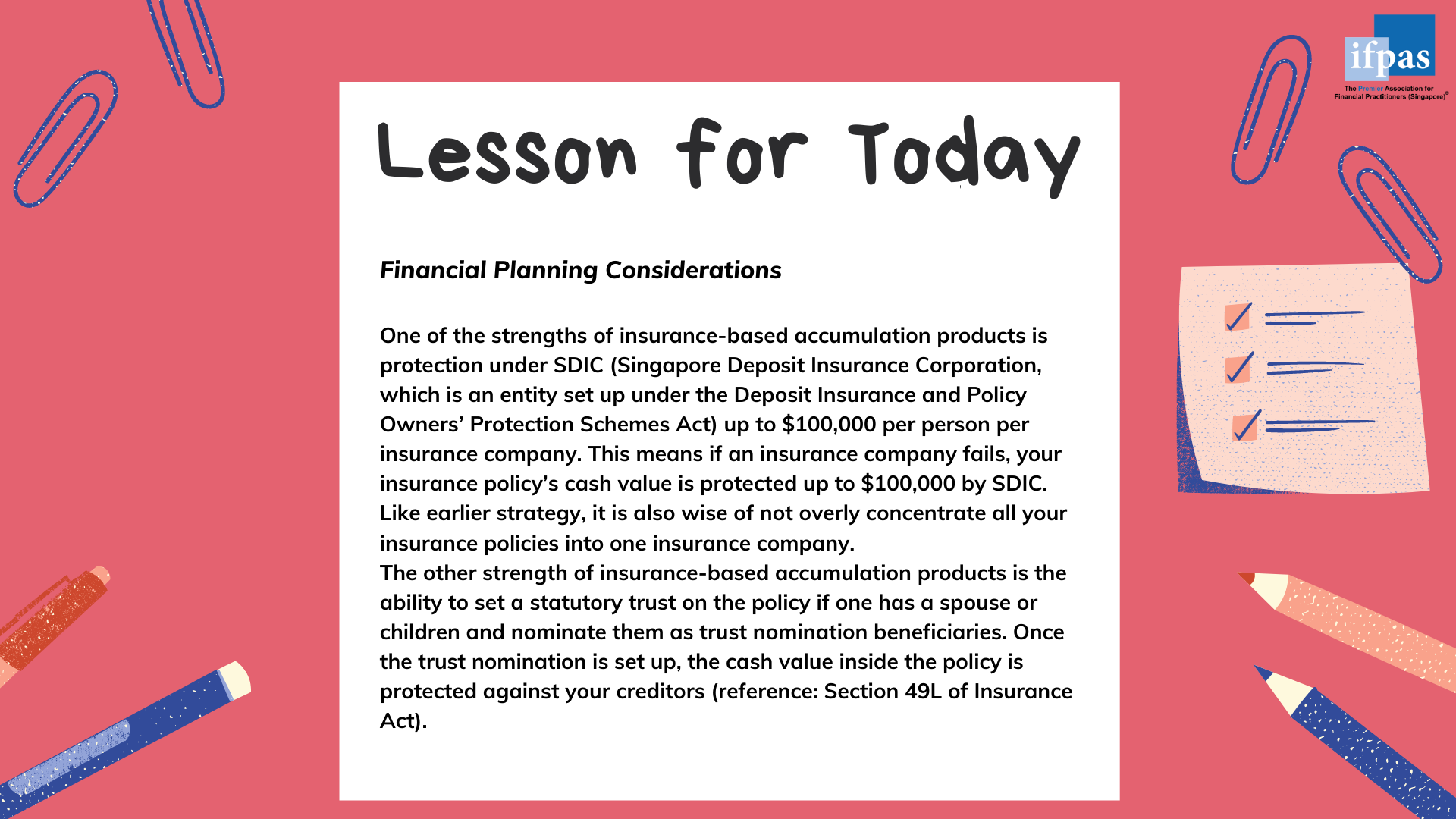

Financial Planning Considerations – It is important to start accumulating assets early for your future self. As in all planning, one needs to be discipline, and make hard choices on current consumption. The following table shows the figures needed to accumulate S$1M at age 65 based on a weighted average investment return of 4% p.a

| Accumulation Start Age | Yearly Investment Needed (S$) | Financial Goal |

| 25 | 10,119 | To accumulate S$1M at age 65 to generate $60K retirement income per year for 20 years (or till age 85). |

| 35 | 17,144 | |

| 45 | 32,290 | |

| 55 | 80,087 |

The following table shows the effect of unpaid credit debt;

| Initial Debt | S$5,000 |

| Monthly minimum sum payment | S$50 of minim 3% of principal owed (take whichever is higher) |

| Interest rate for overdue outstanding debt | 25% per annum |

| Time taken to pay off all debts | 175 months or 14.5 years |

| Total amount paid eventually | S$13,500 (Almost 3 times the original debt!) |

Financial Planning Tool – Personal Balance Sheet & Investment Summary

It is important to document the assets, debts and investment so that one can keep track on one’s wealth accumulation plan. The presentation is as follows:

Table 1: Personal Balance Sheet

| Personal Balance Sheet for Mr or Ms. XXX (as of date: xx/xx/xxxx) | ||

| Assets | S$ (Market Value) | Ownership Structure (Sole Name, Joint Account etc) |

Cash & Cash Equivalent

|

||

Investment Assets

|

||

Personal Use Assets

|

||

Others

|

||

| Total Assets | ||

| Liabilities (Debts) | S$ (Outstanding amount) | Liable Parties |

Statutory Debts

|

||

Long Term Loan

|

||

Short Term Loan & Others

|

||

| Total Liabilities (Debts) | ||

| Net-Worth (Assets – Debts) | Positive or Negative | |

You have just constructed a personal balance sheet. After this, you can then do a pro-forma balance sheet for next year. The table looks like below:

Table 2: Pro Forma Personal Balance Sheet

| Personal Balance Sheet for Mr or Ms. XXX (year to year) | ||

| Assets | 2019 | 2020 |

Cash & Cash Equivalent

|

||

Investment Assets

|

||

Personal Use Assets

|

||

Others

|

||

| Total Assets | ||

| Liabilities (Debts) | 2019 | 2020 |

Statutory Debts

|

||

Long Term Loan

|

||

Short Term Loan & Others

|

||

| Total Liabilities (Debts) | ||

| Net-Worth (Assets – Debts) | Positive or Negative | |

It is also important to generate a separate investment summary to monitor the investment plans.

| Asset Classes | Start Date | Purchase Value | Current Market Value | Targeted End Date | Targeted Value at End Date | Remarks |

Equity Funds

|

||||||

Bond Funds

|

||||||

Insurance Plans

|

||||||

| Total | ||||||

It is wise to work with a licensed and well-trained adviser to work through these tools. If one equips himself with a personal balance sheet, cashflow statements and investment summaries, one should have a high degree of control over his or her finances. This is an important step towards good financial planning